Why We're Excited about Insurance Premium Finance

Why We're Excited about Insurance Premium Finance

Opportunities to democratize buy now, pay later for insurance and leverage software for insurance billing, integrated banking & payments, and back office

We’ve spent the last few weeks diving into Insurance Premium Finance, essentially a buy now, pay later option for insurance. It’s a $60B+ annual revenue industry in the US that has been dominated by banks for the past few decades. Our takeaway: this is an area that feels ripe for disruption across product innovation, billing and payments, distribution, and integrated banking. Here we’ll dig deeper into what premium finance is, what the market looks like today, growth opportunities, and what we’re excited about in commercial P&C premium finance.

Buy Now, Pay Later for Insurance Premiums

Insurance premium finance is a financial transaction where a third-party provides funds to an individual or business to cover the cost of insurance premiums. Rather than covering the entire premium payment upfront, the policyholder finances the cost of insurance coverage over time in installments. The concept began in the early 1900s when life insurers offered installment plans for policyholders who couldn’t stomach the entire premium upfront.

Rising premium costs and institutionalization of capital markets in the 1970s fueled a formalization of premium finance. In 1983, First Insurance Funding (FIRST) was founded in Chicago to expand premium finance to consumers and business owners. Regulatory changes defined by the FTC and the National Association of Insurance Commissioners (NAIC) in the mid-80’s created product and pricing standards that paved the way for the industry to blossom, leading to the rise of new entrants including Allied Premium Finance, IFCO, and American Premium Finance.

In premium finance, customers can be individual consumers or small and medium-sized businesses (SMBs). For individuals, that means financing premium payments for high cash value life insurance policies. For SMBs, it means financing annual insurance premiums over eight to ten months rather than in a single upfront payment. In both cases, the product is typically distributed through agents/brokers and direct marketing from premium finance companies.

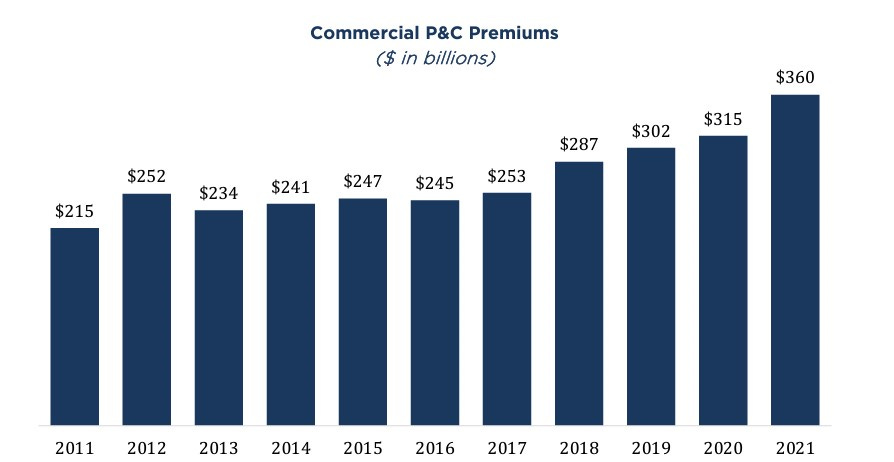

The primary role of insurance premium finance is to help policyholders spread out the cost of their insurance over time. This can be especially impactful for insurance coverages with significant annual costs, which is growing in prevalence in commercial P&C. Premiums have grown at a 5.3% CAGR from 2011 - 2021, adding additional expenses that cut into profitability and prohibit access to optimal insurance coverage. Furthermore, most insurance carriers don’t accept premium payments in installments. Left to their own devices, SMBs often have no choice but to incur the entirety of the cost at the start of the year.

Source: Colonnade Advisors

Commercial P&C Market Dynamics

Commercial lines premium finance is a $45B industry in the US, representing just over 10% of total commercial premiums. In other words, roughly one in every ten policyholders is financing their insurance premiums. The past few years have seen consistent growth, with commercial premiums surpassing personal lines premiums in 2021 for the first time in 10 years. Commercial premium are projected to exceed $600B in the US in the next decade.

For SMBs, the catalyst for premium finance is usually cash flow challenges and mismatches. Facing a challenging macro environment, a common concern from the vast majority of small businesses is over liquidity and access to capital. There’s undoubtedly an opportunity to expand premium finance offerings to a larger portion of commercial policyholders.

Source: APCIA

Amid macro headwinds and the “hard market” in insurance that has persisted over the past few years, rising claims, falling investment income, heightened regulation, and weather-related incidents have posed challenges in the commercial P&C market. That said, there is a counter-cyclical nature to premium finance. Many of the attributes of a hard market exacerbate the demand for premium finance as cash flow and liquidity become paramount concerns for small businesses.

What Incumbents Get Right

Legacy premium finance companies and regional banks helped to pioneer this market in the late 1980s. They have continued to grow their market share over the past few decades, mostly through consolidation. When you look at the underlying economics, you start to understand why banks and specialty finance companies are holding on tight. This is an attractive credit asset class: short durations, high yields, strong credit quality with historically low loss rates below 1%. On top of that, it’s a secured lending product in the sense that loans are backed by premiums from underlying insurance policies and a sizable down payment of 10-25% premiums. As a result, much of the volume is dominated by deposit-funded banks and specialty finance companies.

Source: Moody’s

The advantages that incumbents have are cost of capital (deposits and access to securitization markets), distribution (tenured broker relationships), and market share (bank-led consolidation has amounted to ~60% of the market). At the upper end of the market, much like other parts of financial services, current incentives make the segment difficult to unseat. Relationships matter, and those between premium finance companies and insurance brokers are tightly aligned and reinforced through relationships (i.e. golf), agency commission splits, and renewing existing contracts.

Incumbents are far less focused on the fragmented long tail of the market. Smaller insurance agencies operating through an agency bill model, where insurance agents are responsible for collecting premium payments and paying MGAs or carriers, offers opportunities to democratize the premium finance to SMB customers who are historically overlooked.

Source: Colonnade Advisors

To an early stage investor, it feels like a market ripe for disruption with the presence of legacy banks and specialty finance companies with little in the way of modern technology, AP/AR automation, payments processing, or data integrations. Add to that the complex back end payments, reporting, and reconciliation that lives in siloed spreadsheets and agency management systems (AMS). We believe there are a number of industry characteristics that present interesting opportunities for product, payments, and distribution innovation.

Where We’re Spending Time

We believe there is opportunity to broaden access to premium finance for small businesses of all shapes and sizes. We’re most excited about the models attacking it with a focus on back office management, payments orchestration, and data automation combined with premium financing offerings.

Competing with a credit-first approach is not the right strategy given the cost of capital advantage held by incumbents. However, there are a number of opportunities to expand the ecosystem and build back office software and payments products with premium finance as a core value proposition. Companies like Ascend and Functional Finance have focused on software and payments alongside premium finance, and expanding distribution in a more fragmented sections of the market (smaller agencies and MGAs, respectively). Taking it one step further, integrating a vertical neobank product and for insurance agencies and MGAs that’s tied to premium finance and payments offerings feels like a large opportunity that we want to explore further.

As investors in a number of software-led lending businesses, we’re excited about the software-led applications in premium finance to improve agency efficiency, enhance coverage availability for SMBs, and to create industry-specific products in markets with unique needs and dynamic coverages such as e-commerce, gaming, cannabis, and other dynamic industries. We’re also excited about pay-as-you-go pricing models where policyholders can tailor their insurance coverage based on the dynamic facets of their business, as opposed to a static view determined at the end of the year.

As a hybrid fund, we invest credit and equity together in technology companies with a capital intensive element. If you are building or thinking about opportunities at the intersection of insurance, payments and premium finance, we’d love to meet you. Feel free to reach out to me at Conor@upper90.io.

Notice to Recipients:

This document is for informational purposes only and should not be relied upon as investment advice. This document has been prepared by the Upper90 Capital Management and is not intended to be (and may not be relied on in any manner as) legal, tax, investment, accounting or other advice or as an offer to sell or a solicitation of an offer to buy any securities of any investment product or any investment advisory service. the information contained in this document is superseded by, and is qualified in its entirety by, such offering materials. This document may contain proprietary, trade-secret, confidential and commercially sensitive information. U.S. federal securities laws prohibit you and your organization from trading in any public security or making investment decisions about any public security on the basis of information included in these materials.

This document is not a recommendation for any security or investment. references to any portfolio investment are intended to illustrate the application of the Upper90 Capital Management’s investment process only and should not be used as the basis for making any decision about purchasing, holding or selling any securities. nothing herein should be interpreted or used in any manner as investment advice. The information provided about these portfolio investments is intended to be illustrative and it is not intended to be used as an indication of the current or future performance of Upper90 Capital Management’s portfolio investments.

An investment in a fund entails a high degree of risk, including the risk of loss. There is no assurance that a fund’s investment objective will be achieved or that investors will receive a return on their capital. investors must read and understand all the risks described in a fund’s final confidential private placement Memorandum and/or the related subscription documents before making a commitment. The recipient also must consult its own legal, accounting and tax advisors as to the legal, business, tax and related matters concerning the information contained in this document to make an independent determination and consequences of a potential investment in a fund, including US federal, state, local and non-us tax consequences.

Past performance is not indicative of future results or a guarantee of future returns. The performance of any portfolio investments discussed in this document is not necessarily indicative of future performance, and you should not assume that investments in the future will be profitable or will equal the performance of past portfolio investments. Investors should consider the content of this document in conjunction with investment fund quarterly reports, financial statements and other disclosures regarding the valuations and performance of the specific investments discussed herein. Unless otherwise noted, performance is unaudited.

Do not rely on any opinions, predictions, projections or forward-looking statements contained herein. Certain information contained in this document constitutes “forward-looking statements” that are inherently unreliable and actual events or results may differ materially from those reflected or contemplated herein. Upper90 Capital Management does not make any assurance as to the accuracy of those predictions or forward-looking statements. Upper90 Capital Management expressly disclaims any obligation or undertaking to update or revise any such forward-looking statements. The views and opinions expressed herein are those of Upper90 Capital Management as of the date hereof and are subject to change based on prevailing market and economic conditions and will not be updated or supplemented.

External sources. certain information contained herein has been obtained from third-party sources. Although Upper90 Capital Management believes the information from such sources to be reliable, Upper90 Capital Management makes no representation as to its accuracy or completeness.

This document is not intended for general distribution and it may not be copied, quoted or referenced without the Upper90 Capital Management's prior written consent.